The numbers are in, and for millions of Americans relying on Medicare, 2026 is shaping up to be a year where the fine print matters more than ever. The Centers for Medicare and Medicaid Services (CMS) dropped the details on Friday, November 14th, and if you’re trying to make sense of your retirement budget, you’re going to want to pay close attention. Because while the official line might sound reassuring, the data, as it always does, tells a more nuanced story.

The Shrinking Slice: Part B Premiums and Your Social Security COLA

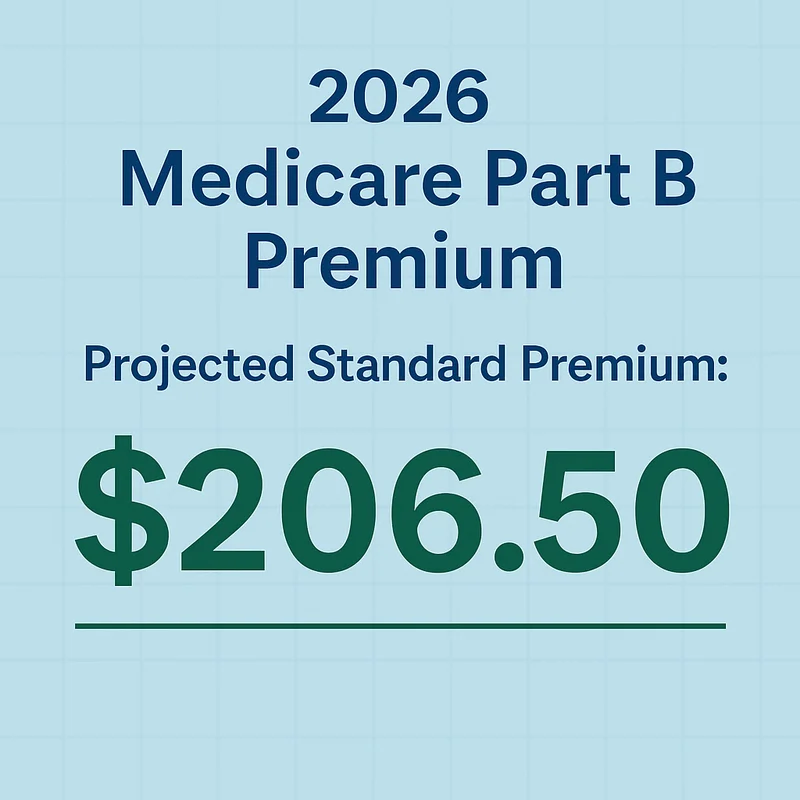

Let's start with the headline grabber: the standard monthly Medicare Part B premium for 2026 will hit $202.90. That's an increase of $17.90 from 2025, or nearly 10%. Now, stack that against the 2026 Social Security increase – a 2.8% cost-of-living adjustment (COLA), which translates to an average bump of $56 per month for someone receiving around $2,008. Do the math, and you'll see that Part B premium hike will consume nearly one-third of that average COLA. Medicare premium increase reduces Social Security COLA for 2026 - USA Today. To be more exact, it’s 32% right off the top.

Imagine the collective sigh across dining room tables as seniors, many on fixed incomes, pore over the notices from CMS. For lower-income Social Security beneficiaries, say those receiving $600 a month, their COLA increase of $16.80 is actually less than the Part B premium hike. This isn't just a rounding error; it's a direct financial hit.

Now, CMS will point to the "hold harmless" provision, and it's true: this will protect some Social Security recipients with benefits of $640 or less, limiting their Part B premium increase to the dollar amount of their COLA. That’s a good thing, a necessary buffer, but it also underscores the underlying pressure. It's like a small umbrella in a sudden downpour – it keeps some rain off, but the storm is still raging.

And if you're a higher earner? Your medicare premiums based on income 2026 will jump even more. Single beneficiaries with adjusted gross income (AGI) over $109,000, or married couples over $218,000, will see their Part B costs climb significantly. A couple with modified AGI between $274,000 and $342,000 could be looking at $405.80 per month for Part B alone. My analysis suggests that while these income-related adjustments have been around since 2007, the widening gap between standard and high-income premiums creates a distinct, dual-track system. We're also seeing the second-largest dollar increase in Part B history, trailing only 2022's $21.60 jump. This isn't an anomaly; it's a trend, driven by rising medical costs and the ongoing shift of services to outpatient facilities, which fall under Part B.

The Shrinking Advantage: Fewer Choices, Higher Costs

While Part B grabs headlines, the changes coming to Medicare Advantage (MA) plans are equally, if not more, concerning. The number of Medicare Advantage offerings is decreasing by a solid 10% for 2026, down to 3,373 plans. Major insurers like CVS Aetna, Elevance (which is also exiting the Part D market), Humana, and UnitedHealthcare are reducing plan options in at least 100 counties, impacting over 2 million people. In a stark first, some Americans, for example in eight Vermont counties, will have zero Medicare Advantage plans available.

Dr. Mehmet Oz, the CMS administrator, stated that millions of Medicare beneficiaries will continue to have access to a broad range of affordable coverage options in 2026. But I've looked at hundreds of these filings, and this particular footnote is unusual: when the average number of MA plans available to beneficiaries drops from 42 to 39, and entire counties lose all options, how do we define "broad range"? Fewer plans will offer $0 premiums, fewer PPO plans (which typically mean wider provider networks), and fewer will offer $0 deductibles for prescription drugs. It’s like a game of musical chairs, but the organizers keep quietly removing a few seats each round while assuring everyone there's still plenty of room.

And let's not forget the financial squeeze within MA itself. Maximum out-of-pocket limits for medical care are rising by an average of $490 (approximately 10%). The average premium for MA plans with drug coverage will increase to $66 in 2026, up from $60 in 2025. Even the supplemental benefits, often touted as a major draw for MA, are becoming less generous; the average dental allowance, for instance, is declining 10% to $2,107. The current overhaul in the Medicare Advantage market is clearly driven by medical costs outpacing reimbursements from the federal government to insurers. The insurers aren't trying to grow; many are pulling back, as noted by Greg Berger from Oliver Wyman.

So, while the official press releases paint a picture of continued choice, the raw data points to a significant contraction. What happens when "broad range" shrinks to just a handful of viable options, particularly in rural areas? And what's the long-term solvency strategy here beyond these annual adjustments that chip away at seniors' fixed incomes? The annual Medicare open enrollment period ends December 7, and these numbers should be front and center for anyone making decisions.

The Numbers Don't Lie: A Squeeze, Not a Solution

The 2026 Medicare announcements, especially concerning medicare part b premiums, lay bare a fundamental challenge. Medicare Just Announced Its 2026 Premiums, and It's Bad News for Social Security's Dual Enrollees - Yahoo Finance. Despite the welcome, albeit modest, 2026 Social Security increase, the escalating cost of healthcare is creating an undeniable financial squeeze for seniors. The official narrative, while emphasizing choice, doesn't quite align with the quantifiable reduction in options and the very real increase in out-of-pocket costs. We're not just kicking the can down the road; we're asking seniors to shoulder more of the burden. It’s a reality check, plain and simple, and it demands more than just hopeful rhetoric.